Over 50 with no solid retirement plan? Consider the answers to these 6 questions.

When I talk to clients in their 50s and 60s, many of whom are heading towards retirement, the most common sentiments I hear are “I need to act quickly, but I’m not sure what to do” or “Everything’s changing so fast. I should wait until things settle down.” In reality, neither approach is ideal. Rash decisions in response to changing legislation or share market noise may not be wise, but doing nothing isn’t much help either.

When I talk to clients in their 50s and 60s, many of whom are heading towards retirement, the most common sentiments I hear are “I need to act quickly, but I’m not sure what to do” or “Everything’s changing so fast. I should wait until things settle down.” In reality, neither approach is ideal. Rash decisions in response to changing legislation or share market noise may not be wise, but doing nothing isn’t much help either.

So what can we do in response to the inevitable volatility, change and uncertainty that comes with economic transformation? I think the key is to seek good advice and make more frequent adjustments to your plan of attack, with a firm focus on wealth maximisation.

Is it time to rethink the transition to retirement?

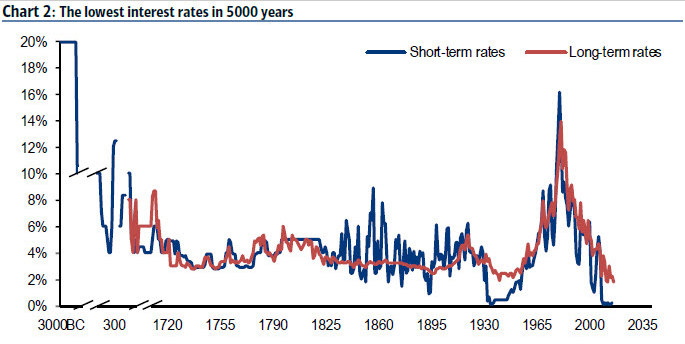

The short answer is yes. Low growth on savings and investments are becoming all-too-familiar and the fact we now have the lowest global interest rates since time began – see chart below – indicates that this is going to be a challenge for some time.

Source: BofA Merrill Lynch Global Investment Strategy. BoE Global

Source: BofA Merrill Lynch Global Investment Strategy. BoE Global Financial Data, Homer and Sylla "A History of Interest Rates'.

You may be looking to scale down your working hours, but the reality is many people will need to work longer than planned to accumulate the savings they need to maintain their lifestyle - or even to adopt a more modest lifestyle. If slowing down is a priority, my advice is to re assess your lifestyle to suit your current and expected level of income, and explore ways of restructuring your hours and remuneration. I recently heard a great example of this in the public sector where some employees can ‘buy’ extra leave in exchange for a lower overall annual salary. This can be used to create a four day week or longer travel break, which in turn may extend your working life. For those in business, it could be worth rethinking succession planning strategies – more on that in next week’s email for business owners.

How do I deal with the changing economy?

There are a couple of things to consider here. Firstly, the change from the old economy to the new, how will this happen and how do I invest so I don’t lose the lot by jumping too early into the new, or staying too long in the old? The second aspect is the broader impact of economic change. We have already mentioned the low earnings environment, we also need to have a weather eye on things such as inflation and deflation. A plan for a deflationary environment would be different to an inflationary environment. If we expect deflation we would consider retiring debt earlier, and moving a greater proportion of our assets to cash. If we expect an inflationary environment we would defer repaying debt and have less of our asset pool in cash.

We continually note that retirement is more likely to be longer, so we ought to take a long term view. A long term view does not mean set and forget, in my view it means regular

reassessment and review.

Do I need to start being selfish with my money?

Definitely! Some people I talk to about retirement planning still aim to supplement their superannuation income stream with the Age Pension to achieve a reasonable standard of living, and maybe gift some savings to their kids or grandkids. Those that do not qualify for the age pension also need to consider their individual position. Once given away, assets cannot be easily retrieved. Retirement is now about a longer term investment strategy. Many of us will live for 30-35 years past retirement, so the slow and steady approach to drawing an income stream is not going to be enough. It’s not so much about being selfish but seeking advice, thoughtfully managing assets and having a plan. I’m not suggesting taking unnecessary risks, but the focus should remain on growth.

Can I really count on the Aged Pension?

Not necessarily. It is likely there will always be some form of government safety net, but it is hard to predict how much and for whom. New legislation from January 2017 will already reduce overall Age Pension eligibility [Essentially, the new measures will decrease the asset test threshold, and will also double the amount by which the pension reduces for every $1000 you have above the threshold. Depending on your situation, it may be difficult to get the pension or you might receive less] and we can expect the government to keep reforming the pension in this way to ultimately support those with lower income and fewer assets. Another reason to be proactive about growing your retirement savings, even in retirement.

How do I want to live in the next phase of life?

Each of our clients has unique aspirations and objectives for retirement. So when I sit down with them to review their retirement plan and investment strategy, a key focus is lifestyle priorities. If you love cars and want to drive a Mercedes-Benz, that's fine – but it might mean you can’t afford an overseas holiday every year too. The bottom line is retirement savings have to last longer than many people first think, so I encourage a mindful reassessment of what really matters. That also means thinking about a sense of purpose. It’s great to look forward to tackling the bucket list once you have more time, but people who’ve retired will tell you, that novelty lasts a year or two and there’s a lot of living to do after that. It’s not just how you’ll make your money last that you have to consider, but how you’ll spend your time.

There is certainly a lot to think about and the turmoil of economic transformation can leave many unsure what, if anything, they can do to protect their financial future. My advice is have the confidence to keep making plans, but revisit them more often and seek professional expertise to make the necessary adjustments to reach your goals.

If you’d like to review your plans or have any other concerns, I'm happy to help.